Now that the election is behind us, I feel more settled, and I suspect many investors do too. Hopefully, the markets will respond in kind. It's been a stressful roller coaster ride for investors recently. No one enjoys watching their portfolio value dip, but thankfully, dividends continue to be paid out even when the stock prices fluctuate. That steady income is a welcome comfort during these times of volatility.

This was especially eye-opening for our kids. After dabbling in some U.S. growth stocks and seeing them drop significantly, they’ve come to appreciate the power of dividend-paying stocks. It gave my husband and I the perfect opportunity to highlight how reliable dividend-growers are, regardless of market swings. In fact, the kids even received a few dividend increases over the past few months, which really drove the message home: consistent, growing dividends can be a powerful wealth-building tool.

Honestly, I think my husband was more stressed than the kids about their growth investments! But with time on their side, the kids can afford to wait it out—and learn some valuable lessons in the meantime. They've started to consider valuation, and how overpriced stocks can often face a reckoning later on down the line. Thankfully, their exposure to riskier stocks was minimal, but the experience was a great reminder of why dividends, while maybe less exciting to the younger generation, offer long-term growth with less risk and less stress.

If you're considering adding dividend stocks to your portfolio, here are a few key benefits to keep in mind:

Dividend Reinvestment

One of the greatest advantages of dividend investing is the compounding effect. When you reinvest dividends to purchase more shares, your investment can grow exponentially over time. You may have heard dividend investors talk about the “snowball effect”—this is exactly what they mean. The more shares you own, the more dividends you receive, which in turn buys more shares, and the cycle continues. Over the years, this simple habit can lead to significant portfolio growth.A Source of Income

Let’s not forget that dividends are a true income stream. This becomes especially valuable in retirement, but really, it’s helpful at any stage of life. Even when markets are down, as we’ve seen recently, dividend payments often continue like clockwork. That steady income can provide peace of mind. And if you don’t need the income right away, reinvesting those dividends accelerates your portfolio’s growth potential even more.Less Volatility

Dividend-paying stocks tend to be less volatile than non-dividend payers. Why? Because many dividend-paying companies are well-established, with strong fundamentals and consistent earnings. Investors value that stability, especially during uncertain markets, which helps keep these stocks more resilient. In fact, when prices dip slightly, long-term investors often view that as a buying opportunity.An Inflation Hedge

Dividends can act as a powerful hedge against inflation. If inflation rises by 2% annually, and your dividend-paying companies are increasing their payouts by 5%, you're not just keeping pace—you’re growing your purchasing power. Over time, this can make a substantial difference in maintaining your standard of living.Total Return = Dividends + Price Appreciation

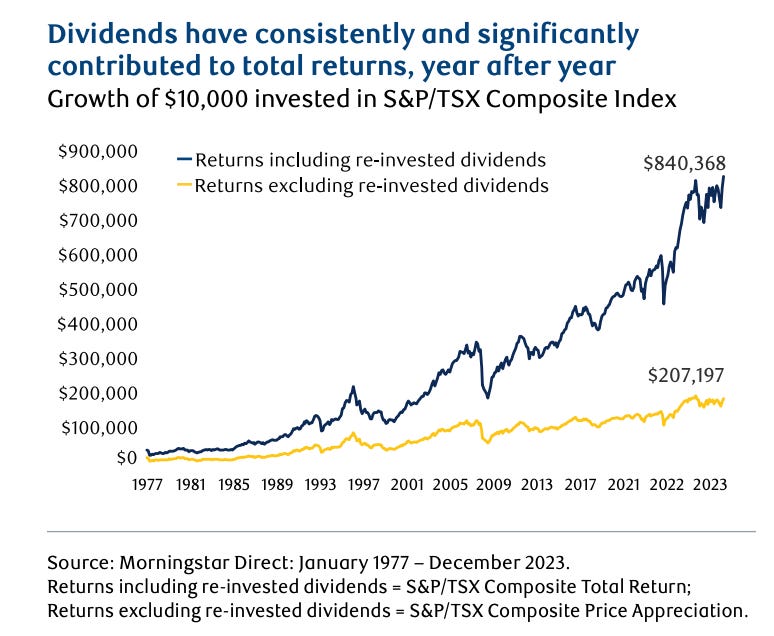

Dividend-paying companies contribute meaningfully to long-term total returns. Historically, a significant portion of the market’s return has come from dividends. Not only do you benefit from capital appreciation, but you also receive ongoing cash payments. If you hold quality dividend growers long enough, there may come a day when the total dividends you’ve received exceed your original investment—something many seasoned dividend investors have experienced.Here’s a chart from RBC that illustrates just how impactful dividend reinvestment can be over time. Even modest reinvested dividends can dramatically enhance long-term total returns thanks to the power of compounding.

Check out: The Power of Dividends from RBC

To DRIP or Not to DRIP? That is the Question

If you hold dividend-paying stocks, you can ask your brokerage to enroll you in an automatic Dividend Reinvestment Plan (DRIP). This means your dividends will automatically be used to buy more shares of the same company—commission-free. It’s a convenient way to grow your holdings, but there are a few things to keep in mind.

First, your dividend must be large enough to purchase at least one full share. Second, every DRIP transaction affects your average cost base, either increasing or decreasing it. For these reasons, I’m selective about which companies I enroll in a DRIP.

Here are a few factors I consider before enrolling a company:

How many shares I already own: If I hold a significant number of shares, I might prefer to use those dividends to diversify into another company rather than automatically reinvesting.

Current stock price vs. my cost basis: If the share price is significantly higher than when I first bought the stock, I often hold off on DRIP. Instead, I’ll use accumulated dividends to buy companies that are more attractively valued. For example, a few months ago I used dividends from other holdings to buy more BMO shares after the stock price dropped—rather than having it enrolled in a DRIP and my brokerage buying shares every quarter when the price was higher.

Account type: I’m more likely to use DRIP in my TFSA. Since I aim to max out my TFSA contributions in January each year, I can’t add new funds during the rest of the year. My brokerage charges $9.99 per trade, so DRIP helps me build my position gradually and commission-free.

If you’re using a platform like Wealthsimple that offers commission-free trading, you may prefer to reinvest dividends manually—giving you full control over where and when to invest. That flexibility is a major advantage.

Why Dividend Stocks Make Sense for a Stable Portfolio

Regular Income

Dividend-paying companies return a portion of their profits to shareholders—often quarterly—providing a steady income stream regardless of market swings.Lower Volatility

Dividend stocks, especially from blue-chip names like banks, utilities, and insurers, tend to be less volatile than high-growth or speculative stocks. Their mature business models and reliable cash flow provide greater price stability.Downside Protection

In down markets, dividends help cushion the blow. Even if the stock price declines, you're still earning income, helping to preserve portfolio value.Compounding Power

Reinvested dividends boost growth over time, especially when combined with companies that consistently raise their payouts. This creates powerful compounding potential.Signals Strength

Companies that consistently grow their dividends typically have strong balance sheets and disciplined management—traits that contribute to long-term success.Psychological Stability

Knowing your investments are generating income even during market downturns can help you stay the course and avoid panic selling. This is one of the key aspects that draw many investors to dividend paying companies.

In short, dividend stocks appeal to a range of investors—retirees looking for income, conservative investors seeking lower volatility, and long-term investors focused on compounding growth. Whatever your goal, dividend investing can provide a solid foundation for a resilient portfolio.

Building a Portfolio? Here’s a Sampling of Some Canadian Dividend Stocks:

Financials:

Royal Bank of Canada (TSX: RY)

Dividend Yield: ~3.5%

Highlights: Canada’s largest bank with a strong history of dividend growth.

It’s never a bad day to buy Royal Bank in my opinion.

Bank of Montreal (TSX: BMO)

Dividend Yield: ~4.7%

Highlights: Consistent dividend increases; recently raised its quarterly dividend by 2.6%

Analysts feel the stock is undervalued and have upgraded the target price to $155. The current price is $134.84

Power Financial (TSX: POW)

Dividend Yield: ~4.7%

Highlights: Strong performance in 2024; considered undervalued by some investors

Analysts in March 2025 upgraded the target price of the stock to $62 vs the previous $56 per share. The current price is $51.35

Utilities:

Fortis Inc. (TSX: FTS)

Dividend Yield: ~3.6%

Highlights: Known for 50+ consecutive years of dividend increases; a staple for conservative portfolios.

The average target price from analysts is around $65 and this is a solid well-run company.

Enbridge Inc. (TSX: ENB)

Dividend Yield: ~5.8%

Highlights: 30-year track record of dividend increases; transports 30% of North American crude oil.

“TD Securities has reiterated its “Buy” rating on Enbridge maintaining a 12-month price target of CAD $67, which implies a modest upside from the last closing price of” $64.73

TC Energy Corp (TSX: TRP)

Dividend Yield: ~6%

Highlights: Operates critical energy infrastructure; offers stable cash flows.

From the Globe and Mail this week: TC Energy expanding U.S. gas network to fuel data centre growth in Midwest

Energy:

Suncor Energy (TSX: SU)

Dividend Yield: ~4.5%

Highlights: Raised dividend by almost 5% in late 2024; strong production growth.

I’ve been a proponent of Canadian Oil and Gas stocks for a very long time. Despite the drop in the WTI price I believe Suncor (and CNQ below) are good long-term holds.

Canadian Natural Resources (TSX: CNQ)

Dividend Yield: ~5.8%

Highlights: Consistent dividend growth; solid balance sheet, exceptional management team.

“In a research report released Friday titled Crazy Train, equity analysts at National Bank Financial reiterated their “optimistic” view of the long-range opportunities available to investors across Canada’s energy sector, while they acknowledge short-term turbulence is likely to persist with recent news flows feeling like “a never ending tilt-a-whirl.”

“The analysts lowered their target prices for stocks by an average of 6 per cent after reducing their 2025 and 2026 cash flow estimates by 10 per cent and 11 per cent, respectively, due to broad revisions to their 2025 and 1H26 commodity price assumptions (in particular crude) to better align with forward strip.”

Other:

Savaria Corporation (TSX: SIS)

Dividend Yield: ~3.0%

Highlights: Provides accessibility solutions; steady dividend payer.

In March, “Desjardins Securities’ Frederic Tremblay lowered his Savaria Corp. (SIS-T)target to $25 from $27 with a “buy” rating. Other changes include: Raymond James’ Michael Glen to $24 from $27.50 with an “outperform” rating, Stifel’s Justin Keywood to $24 from $25 with a “buy” rating, Scotia’s Jonathan Goldman to $22 from $25 with a “sector outperform” rating and National Bank’s Zachary Evershed to $24 from $27 with an “outperform” rating. The average is $25.93.

“While potential tariff impacts prompted management to temper its 2025 outlook, we are confident that Savaria has the necessary operational and financial resources to navigate this short-term turbulence,” said Mr. Tremblay. “The goal of reaching the coveted 20-per-cent margin level may be slightly delayed, but it is certainly not forgotten — it remains top of mind across the organization, and management hinted at the potential to first reach it as early as 2H25. We are maintaining our Buy recommendation.”

The current price is $17.81

Our Dividend Income for April

We came so close to breaking the $6,000 mark in dividends for both January and April—but it looks like we’ll have to wait just a little longer. For April, our total dividend income came in just shy of $5,900.

That still represents a strong year-over-year increase of more than 7% compared to last April, which is a milestone worth celebrating. Steady growth like this reinforces the power of dividend investing and the value of staying the course.

Remember earlier when I talked about how investing in solid dividend-paying companies can help hedge against inflation? Well, here’s a real-life example: several of the companies I own have already increased their annual dividends for 2025.

That means I’m earning more income this year than I did last year—without adding a single extra share to my portfolio. It’s one of the best features of owning dividend growers: your income keeps rising, even if you don’t invest additional capital.

AltaGas increased dividend by 6%

Atco by 3%

BMO by 2.6%

CNQ by 4.4%

Canadian Utilities by 1%

Enbridge by 3%

Extendicare by 5%

Manulife by 10%

Power Corp by 9%

Royal Bank by 4%

Suncor by 4.6%

TC Energy by 3.3%

TD by 2.9%

Telus by 3.4%

Tourmaline by 43%

Our Transactions in April

We recently made a few changes to our portfolio—selling our position in Cenovus and reallocating those funds to add more shares of Royal Bank, Canadian Natural Resources (CNQ), and Telus. We also initiated a new position in Wajax.

Wajax is a company with deep roots in Canada, having been founded in 1858—before Confederation. It’s one of the country’s longest-standing and most diversified industrial products and services providers. The company operates through an integrated distribution network that offers sales, parts, and service to a broad range of sectors in the Canadian economy, including:

Construction

Forestry

Mining

Industrial and commercial sectors

Oil sands

Transportation

Metal processing

Government and utilities

Oil and gas

While Wajax didn’t have a strong year in 2024, I believe the current government’s push to invest in Canadian infrastructure and support domestic companies could provide meaningful tailwinds for the business going forward.

From a valuation perspective, Wajax appears undervalued based on the Graham Number. Using the average earnings per share (EPS) over the past three years, the Graham Number calculation values the stock at $40.44 per share (my personal calculations). Using just the most recent EPS, the value comes in at $31.95 (again, all my calculations). For consistency, I use a 3-year average EPS in my analysis chart below, and I’ve added Wajax to the tracking list for reference.

It’s important to note: Wajax would not be considered a dividend-grower, as seen in the chart, specifically the dividend CAGR. This purchase was made primarily for capital appreciation, with the added benefit of collecting a respectable dividend in the meantime.

As of now, four analysts cover the stock—three have it rated as a hold and one as a buy, with an average target price of $20.75.

Our Watchlist and Analysis Chart

Wajax and Savaria have both been added to the chart.

As a reminder, this post, along with any charts or equities discussed, is intended solely for informational and entertainment purposes. It does not constitute a recommendation to buy or sell any of the companies mentioned. Always exercise your own judgment and perform thorough due diligence before making any financial decisions.

Please note that the prices indicated throughout this post as “current stock prices” are at market close on Friday May 2nd.

Calculations in the above chart are my own and there may be errors or typos. Please always do your own research.