Early Retirement and What We Learned About Money Along the Way

Our financial decisions were driven by one simple goal: to retire early and enjoy life. The risks we took to get here paid off, and early retirement has been one of the best decisions we’ve ever made.

While my husband and I earned a decent income during our working years, the most important lesson we learned is this: salary alone doesn’t determine financial success. Yes, a higher income helps—but it’s what you do with your money that truly matters.

Money management is a life skill, yet many people were never taught how to budget, save, or live below their means when necessary. There’s a strong desire to have it all—new cars, stylish furniture, the latest appliances and gadgets, a beautiful home, and luxury travel. But many don’t want to give anything up to get there. The old saying “champagne taste on a Coke budget” still rings true. You may crave champagne, but your finances might only afford you a Coke.

The most valuable financial principle we’ve learned is the age-old advice: live within your means.

We’ve seen people with high incomes fall into the trap of lifestyle inflation, assuming they can afford the latest car or home upgrades simply because of what they earn. But they don’t take into account the full picture—their total expenses, savings rate, or debt load. And often, it’s the lack of awareness that does the most damage.

The truth is, financial freedom doesn’t come from how much you earn—it comes from how intentionally you manage what you have. Whether you’re aiming to retire early, reduce financial stress, or simply have more options in life, it all starts with understanding your money and making it work for you. And one of the best ways to do that is to start investing.

When Should You Start?

The answer is always: now.

There’s no wrong time to start investing, and I encourage everyone to begin—no matter how small the amount. Many people think investing requires a large sum of money, but that’s not true. Anyone can start with what they have.

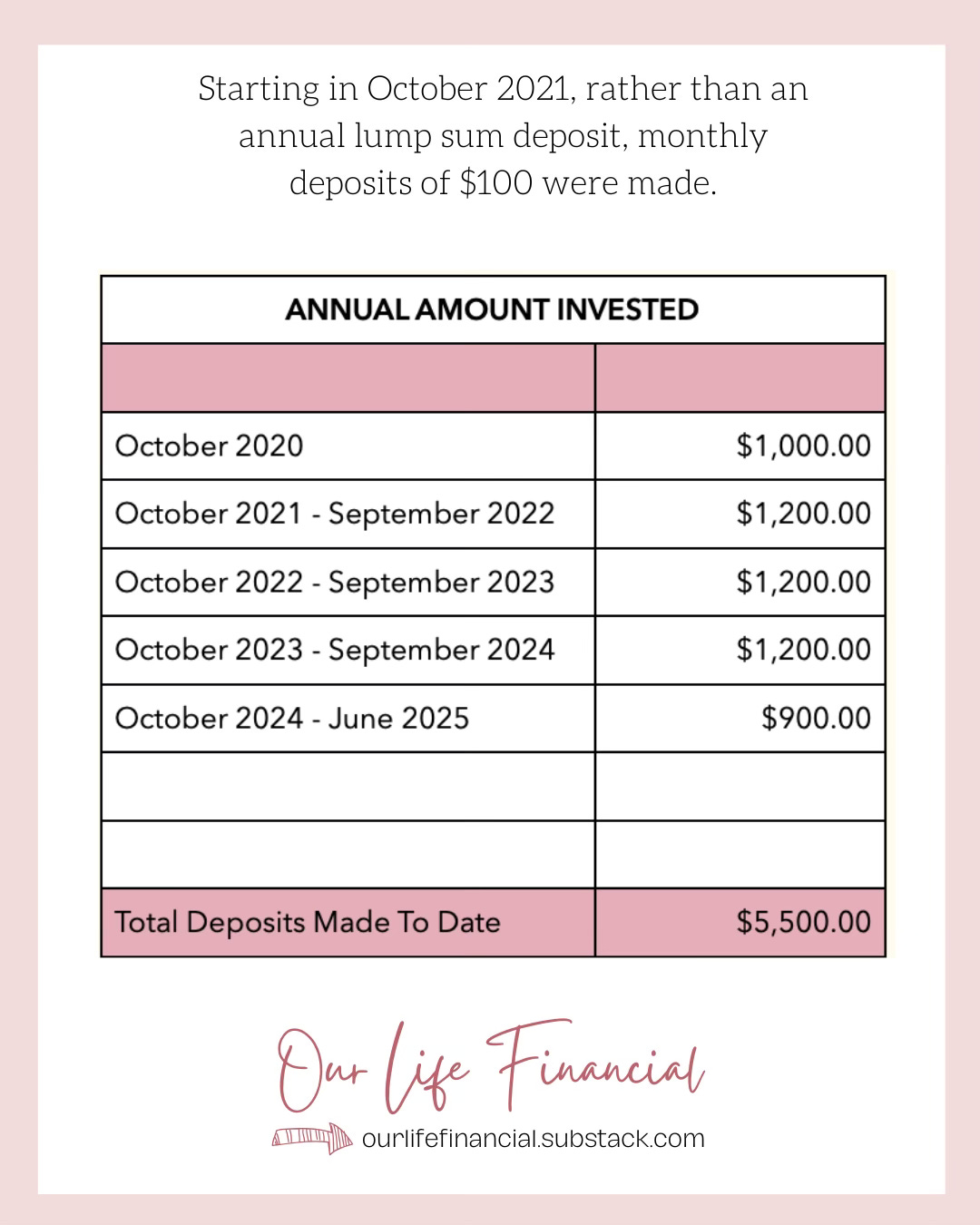

In October 2020, I launched a personal challenge to demonstrate this. I opened a Wealthsimple account to show my Instagram followers how to build a dividend portfolio from scratch. I called it the We Invest Challenge and began with a lump sum of $1,000. I used the entire amount to buy 37 shares of Power Corporation at $26.27 per share. Since then, the investment has doubled in price—and I’ve received consistent dividend income that continues to grow thanks to the company’s annual increases.

The following year, a reader suggested I switch from a one-time annual contribution to monthly deposits. So, in October 2021, I began investing $100 per month, and I’ve kept it up ever since. Today, the We Invest Challenge portfolio is worth more than $11,000. My total out-of-pocket contributions? Just $5,500.

Small Steps, Big Impact

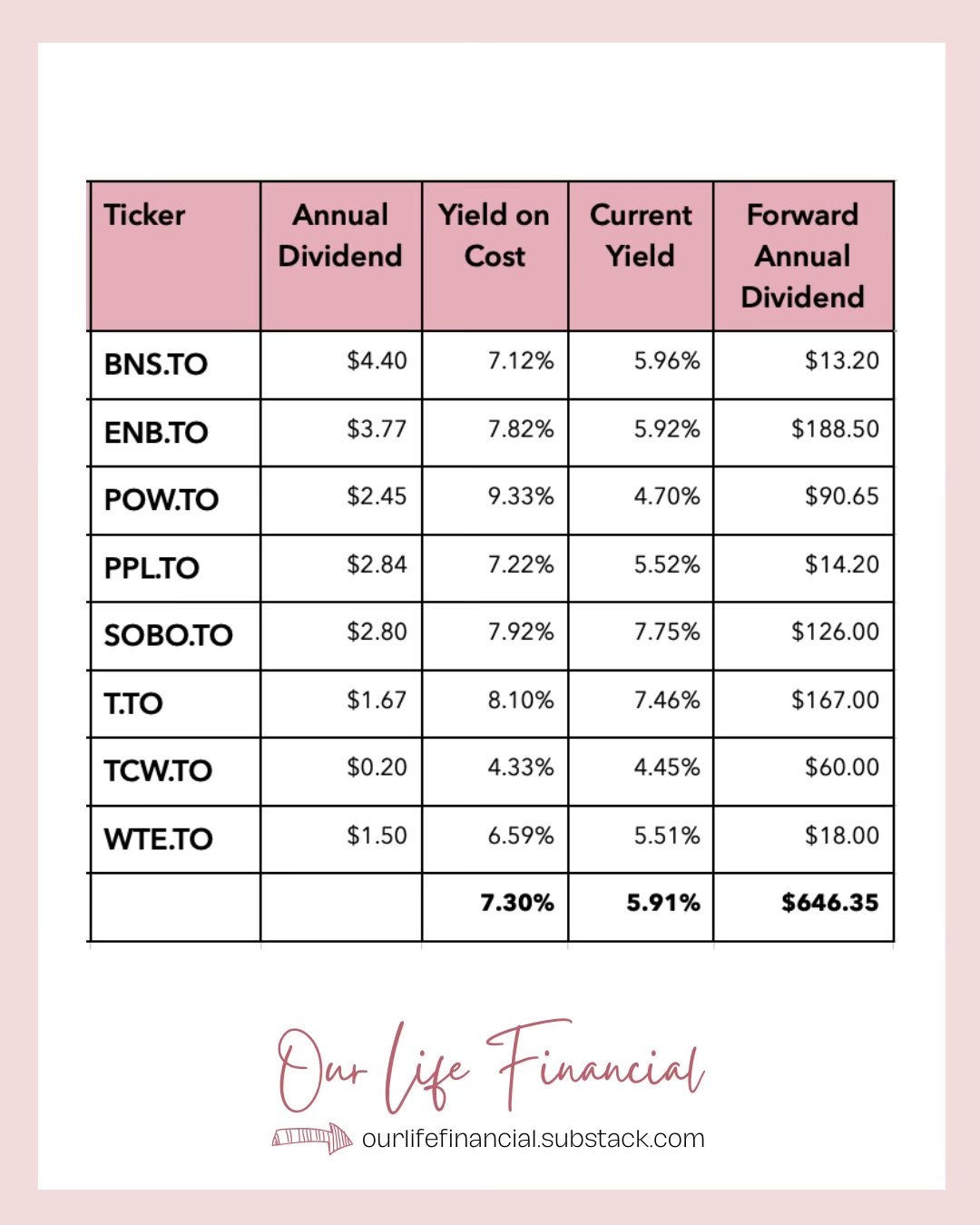

Deposits, capital gains, and dividends have all contributed to the growth of this account, but the primary focus has always been on building a steady stream of dividend income over time. As of today, this portfolio generates $646.35 annually in dividends. I regularly share updates on Instagram, but I wanted to highlight it here because it's an important reminder—especially for new investors—that starting with whatever amount you can is absolutely okay.

You don’t need thousands of dollars to begin investing. In fact, starting small has its advantages: it gives you time to learn, research different companies, and become familiar with the process of buying and holding quality dividend-paying stocks.

Here are a few practical tips to help guide your dividend investing journey:

Not all dividend-paying companies are created equal. Look for businesses with a strong track record of increasing their dividends annually. A minimum of 10 consecutive years of increases is a good benchmark—though the longer, the better. For a quick check, use Yahoo Finance to review the company’s dividend history and confirm the payout has grown consistently over time.

Don’t chase high yields. If a stock is offering a dividend yield between 7–10% (or more), take a closer look. High yields can be a red flag. For example, Bell Canada (BCE) was yielding nearly 14% before it announced a dividend cut, which brought the yield down to a more sustainable 5+%. Dividend cuts hurt your income stream and usually lead to a drop in share price. Many investors saw this coming with BCE, and the stock had been declining for months in anticipation. Even after the cut, investor sentiment remains cautious.

Pay attention to average trading volume. It may seem like a small detail, but knowing how many shares are bought and sold daily can give you insight into liquidity. If a stock has very low trading volume—only a few thousand shares traded per day—you might have difficulty selling your position when needed. Liquidity matters, especially for smaller or lesser-known companies.

Buy when stocks are on sale. Everyone loves a deal, but in investing, getting a good price has an added benefit: a higher yield on cost. For instance, buying a dividend stock at a lower price could mean locking in a 6% yield instead of 5%. That extra percentage compounds over time and boosts your long-term income potential.

Reinvest your dividends. One of the most powerful ways to grow your portfolio over time is by reinvesting dividends. Whether you do this automatically through a DRIP (Dividend Reinvestment Plan) or manually reinvest into new or existing positions, reinvesting helps harness the power of compounding—essentially earning income on your income.

Diversify across sectors. Don’t put all your eggs in one basket, especially when it comes to dividend investing. Aim to hold companies from different sectors like financials, utilities, oil and gas, telecom, consumer staples, and industrials. Diversification helps reduce risk if one industry experiences a downturn or cuts dividends.

Track your income, not just your returns. Dividend investing is about building a reliable income stream, not just watching stock prices. Keep a record of your monthly or annual dividend income to see your progress. Watching your income grow over time is incredibly motivating - especially when prices are volatile.

Stay patient and consistent. Dividend investing is a long game. Some months the market will be up, and others it will be down. What matters is consistency… keep investing, keep learning, and let time do the heavy lifting. Small, steady contributions can lead to meaningful wealth and income over the years.

Remember, successful investing isn’t about timing the market or chasing quick wins—it’s about steady, informed decisions made over time. By starting small, focusing on quality dividend payers, and staying consistent, you can build a portfolio that generates meaningful income and supports your financial goals. Every step you take today brings you closer to the financial freedom you deserve. Keep learning, stay patient, and enjoy the journey.

Our May Dividend Income

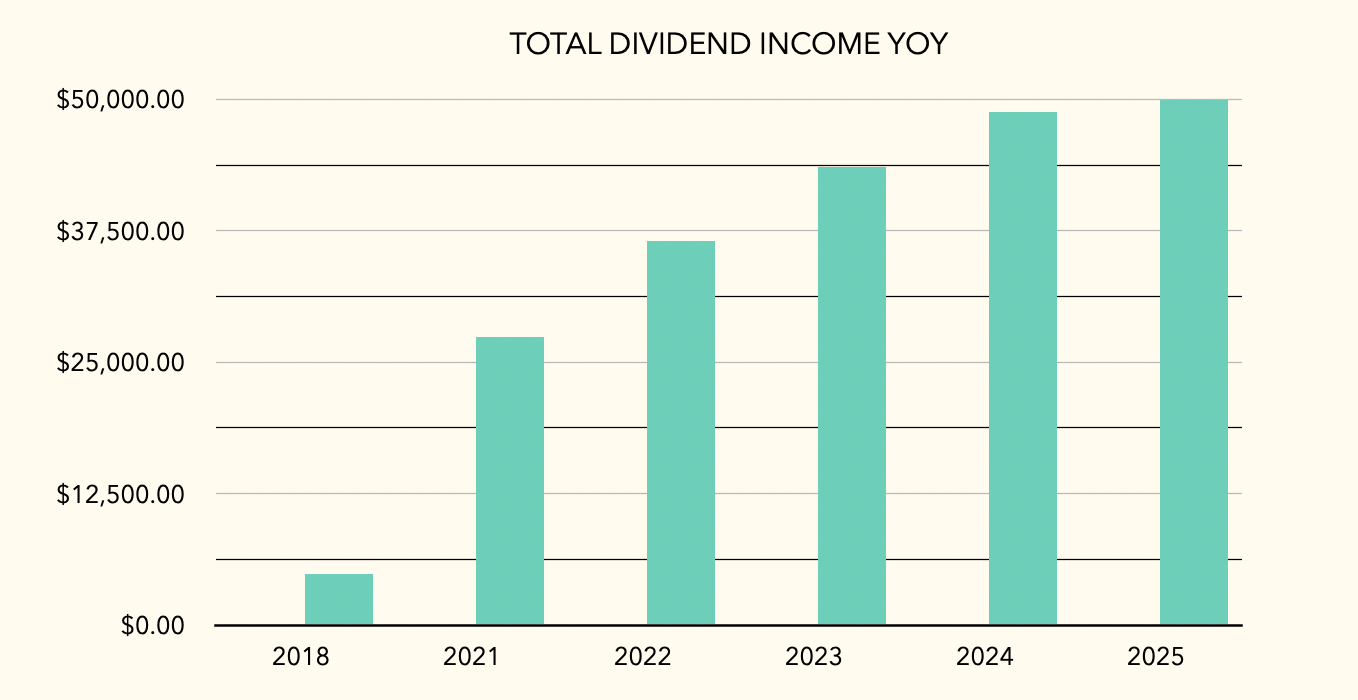

In May we earned just over $2,600 in dividend income. We are happy with the income earned this month as it represents a 15% increase over last May.

We are on track to earn over $50,000 from dividends this year.

*Amount for 2025 is an estimate

My Personal Analysis Chart

As a reminder, this chart is intended solely for informational and entertainment purposes. It does not constitute a recommendation to buy or sell any of the companies listed. Always exercise your own judgment and perform thorough due diligence before making any financial decisions.

Use this chart as a starting point for identifying stocks you may want to research further. Don’t forget, these are companies that I am watching and that your watchlist will/should be different.

Ross Healy Is Not To Be Missed

Amber Kanwar’s podcast just released an excellent interview with Ross Healy—one of my all-time favourite analysts from BNN, though he doesn’t appear as often these days. I haven’t watched the full interview yet, but I’m making myself some tea and setting aside time to listen closely. I’ve always valued his insights.

I saw a snippet of the interview on Amber’s X feed and agree with Ross that a reckoning is on the horizon for the major U.S. tech companies. It won’t just impact the tech giants—many American firms could be caught in the fallout.

Let’s see what Ross has to say about the markets in general and what sectors he believes can provide some solace for the Canadian investor.

Have a listen: