February 2024

A Moment That Changed Everything, Or Did It?.

After Christmas, we decided to tackle the task of cleaning out the basement. A lot can accumulate in 25 years and it’s been on our “to do” list for a very long time.

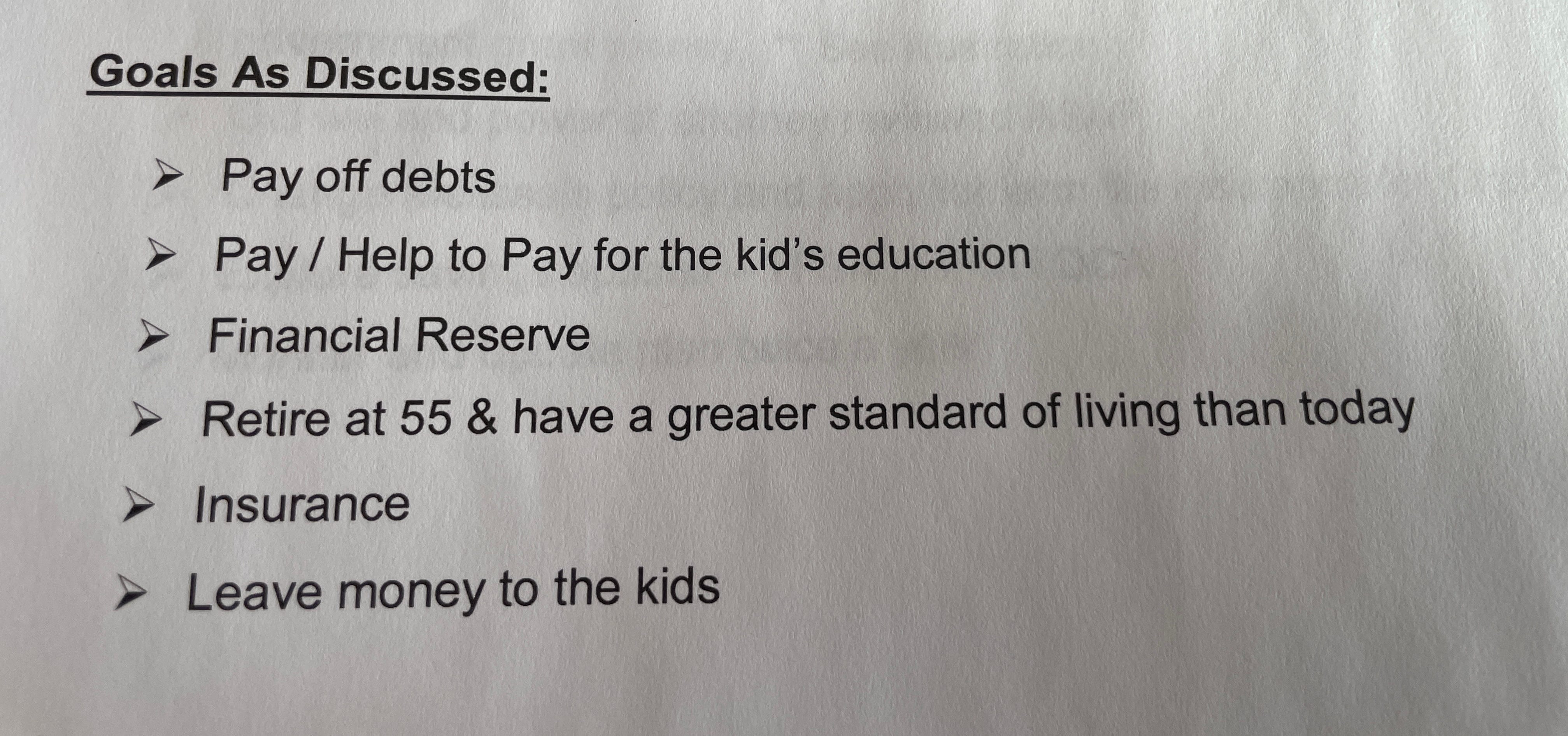

During the purge, I came across some personal papers that had been stored in boxes with various files. One I found interesting was our Retirement Planning Notes provided to us by the one and only financial planner we ever met.

The year was 2009 and I was still in my 30’s. Here are the notes he gave us:

If you’ve been a follower of mine for some time, you may recall me telling you about a meeting we had with a financial planner and how he snickered at our goal of making more in retirement than when we were working full-time. He thought I was ridiculous to even dream of such a thing. This was the financial planner.

He and I were around the same age and maybe the idea of earning more in retirement was a little far reaching, but it still bothers me to this day that he didn’t even consider it a possibility.

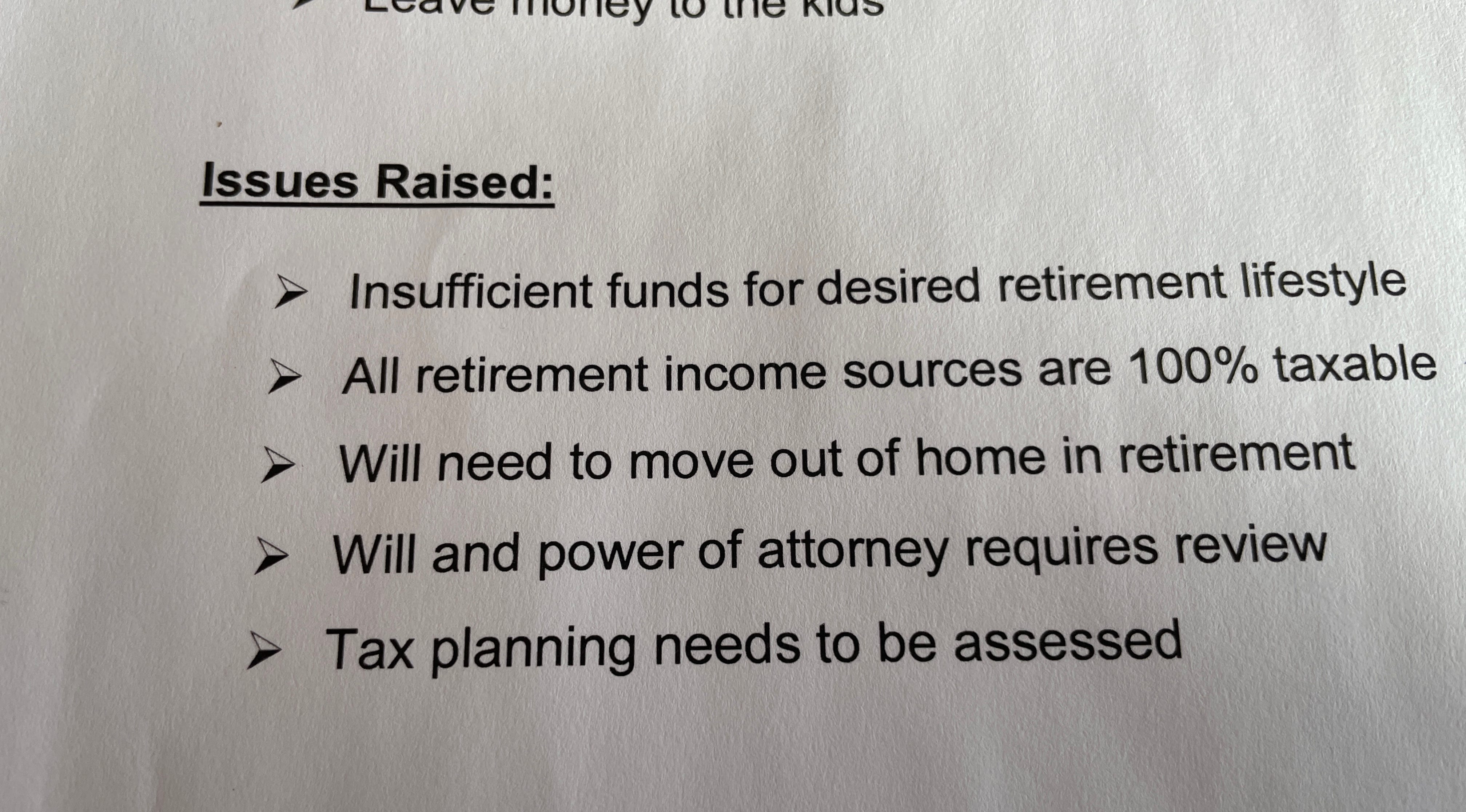

Here are the issues he raised after that meeting:

Probably all legit at the time.

We didn’t have a mortgage on our primary property (we paid it off 6 years earlier). We did, however, have a balance owing on our line of credit that was likely high 5 figures at the time (we purchased a rental property in 2006 for $130,000) and we both had a defined benefit pension plan to look forward to in the future.

I suppose most 30 year olds would have “insufficient funds” for retirement, after all, it was still years away.

He didn’t realize how focused we could be in paying off debt and building our net worth.

Not only did we retire 10 years prior to what he expected, but we didn’t have to move out of our house. In fact, during the last 15 years, we sold the rental property we bought in 2006 to fund a new build in New York State which we rented out on Airbnb. This property was later sold in 2020 during the pandemic. In addition to these properties, we also added a student rental to the mix.

You could say that many risks were taken in those 15 years that were never predicted. Some didn’t work out the way we hoped, but most did. When I look back on our journey, I realize that the financial planner had very low expectations of us.

It still annoys me that he thought I had lost my mind when I said I wanted to retire early and have a higher income in retirement. He couldn’t see it, but I knew it was possible because I watched my parents do it. It’s incredible what can be accomplished when someone is determined especially if you have another person working with you (my spouse).

Maybe after that meeting I became hell bent on proving him wrong. Maybe instead of being annoyed at that memory, I should be thankful he snickered. Maybe… just maybe… that one meeting changed everything.

Interest Rates and Housing

Everyone has been talking about rates coming down, but we all know that the BOC kept rates steady for now.

It still surprises me to hear people predict that even though there was no recent change, the rates “have” to come down. Do they?

I believe the rates will remain high for a very long time. In fact, my generation may never see low rates, like 2-3%, again, which means our kids won’t either. If rates do come down, it may only be a quarter percent, or maybe half a percent if we’re lucky. Do not expect a full percentage point.

Too many people thought low rates were here to stay and splurged in the debt department. Now it’s time to pay the piper. Be careful out there and make sure you can cover debt in the worse case scenario. Even then, have a backup plan.

Our January Dividend Income

We saw a year-over-year increase of 27% in January.